Property investment, when done correctly and with proper guidance, is a wonderful way to supplement your superannuation and pensions while improving your retirement income. Here, we’ve put together a calculator to assist you estimate the additional returns the property can generate.

There are two methods to profit from real estate:

1. Increase in capital

2. Rent

Rental yields in Melbourne are around 3.7 per cent for two-bedroom units and 2.7 per cent for homes, on average, as of January 2022. In comparison to Melbourne, other cities have a higher yield. Nevertheless, Melbourne has had sustained capital growth. Even though address capital growth will not be discussed here, it is undeniable that when the value of the property rises, capital growth becomes increasingly significant.

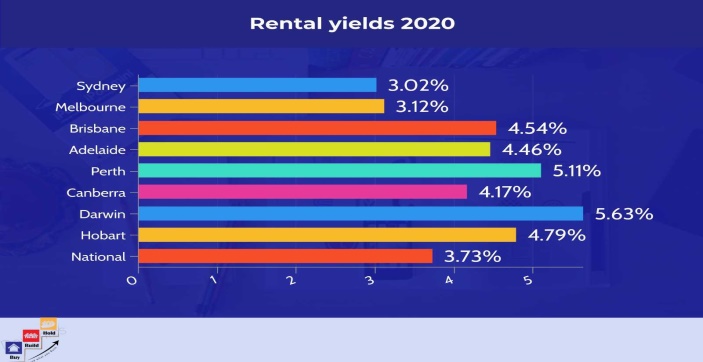

If you spend $1 million in a property with a 3.2 per cent yield, you will receive roughly $32,000 per year in gross income. Let’s say you require $160,000 in income, you would need $5 million in net assets. In simple terms, you’ll need about $1 million in unencumbered property in addition to having your home paid off in full for every $32,000 in net income you plan to have in retirement. Capital growth and living off equity can virtually quadruple this income if managed properly.

Additionally, rent received is one type of income that is referred to as cash flow income from property. When it comes to retirement planning, though, it’s equally critical to understand how equity and capital growth can be leveraged to boost the size of your portfolio and your retirement savings. Needless to say, in most Australian capital cities, the long-term average gross rental income for most property is around 4% of its value (for example, $20,000 per year for a $500,000 property), but the net return after allowing for on-going costs such as agent management fees and maintenance is closer to 2.6 per cent, or $250 per week for a $500,000 property. Because interest on a loan is not included, this is the net rent for a debt-free or unencumbered property.

If you earn 2.6 per cent net, you should get close to $25,000 for every $1 million of unencumbered property, which means you’d need roughly $5 million of property to earn $125,000 in rent alone.

Renting, Investing, and Capital Growth

When compared to renting alone, living off equity and capital growth can significantly reduce the amount of property required to retire or greatly improve your return.

Property should double in value every 12 years, assuming a cautious growth rate of 6% per year compounding (which is lower than the historical average of 9%).

Option 1: Retirement

Keep all of your assets in perpetuity and pass them down to family or charities as an inheritance. You can only live on the average rent of $60,000 per year if you choose this option.

Option 2 for retirement

You should keep only your home for the rest of your life, and pass it down as an inheritance when the time comes. Thereafter, gradually sell your investment properties. For instance, sell one when you reach retirement age, approximately 65, and then another every ten years. If you lived to be 105 and invested the net sale proceeds after selling fees in a managed or superannuation fund with a 6% annual return, you could draw out over $110,000 per year until you died.

Any additional assets and superannuation on top of your property portfolio will, of course, boost your retirement prospects.